Your homeowners' insurance covers the house if a tree falls through the roof. It does not cover the furnace that finally gives out after 14 years of daily use. Or the refrigerator that dies the week before Thanksgiving. Yet these are not rare events; they are the predictable reality of owning a home. The homeowners who handle these moments without financial stress are usually the ones who planned ahead. And a big part of that planning involves understanding home warranty benefits before they ever need to use one.

A home protection plan is straightforward. You pay an annual premium, and when a covered system or appliance breaks down, your provider sends a technician and covers the repair cost. It is protection against the everyday mechanical failures that every home eventually faces.

This guide breaks down exactly what you get, what it costs, and whether home warranties make sense for households.

What are the Primary Home Warranty Benefits for Homeowners?

The benefits of a home warranty go far beyond just fixing a broken system or appliance. A home protection plan creates a financial buffer between you and unexpected repair costs, and saves time and effort. Here is a closer look at what you actually gain.

1. Financial Predictability

This is one of the strongest reasons homeowners invest in a home protection plan. With a warranty, you pay a predictable annual premium and a flat service call fee.

In many U.S. households, HVAC issues tend to show up at the worst time, usually during peak summer. According to a Carrier article, system replacements like HVAC can cost thousands.

What happens without a home warranty?

A homeowner in Texas shared in a consumer review that their AC stopped cooling in July, and the repair estimate came close to $1,400 due to a compressor issue.

With a warranty plan in place, they paid only the standard service fee (around $85), and the rest was handled under their plan. What stood out in their experience wasn’t just the cost savings. It was the ability to move forward with the repair immediately, without comparing quotes or delaying the decision due to budget concerns.

What this means for you:

You are not just saving money. You are avoiding unpredictable expenses during situations that rarely come at a convenient time.

2. Access to Licensed and Experienced Technicians

One of the most overlooked home warranty benefits is access to a vetted network of service professionals. When something breaks, most homeowners spend hours searching for a reliable contractor, collecting quotes, and hoping for the best.

With a home appliance warranty, that process is handled for you. Your provider dispatches a pre-screened technician from their approved network. You do not need to verify credentials, negotiate rates, or worry about the quality of work.

This matters more than most people realize. Hiring on your own can introduce uncertainty in both cost and quality.

What you gain with a provider-assigned service professional:

- Pre-screened and qualified service contractors

- No time spent researching or comparing multiple contractors

- Standardized service rates with no last-minute surprises

- Accountability backed by the warranty provider

- Faster scheduling through an established network

- Support for follow-ups or rework if needed

For busy homeowners or those unfamiliar with home systems, this level of support adds real convenience, making it a strong, often underappreciated advantage of home warranty coverage.

3. Comprehensive Home Systems and Appliances Protection

The breadth of the coverage is one of the most compelling advantages of home warranties. Think about how many systems run quietly in the background of your home every single day. When one of them fails, the disruption is immediate. A warranty ensures you are not forced to prioritize which repair to handle based on what you can afford that month.

Every covered item is treated with the same service commitment. That kind of whole-home coverage creates a genuinely strong safety net for households of any size. Most standard plans are designed to cover the essential systems and appliances homeowners rely on every day.

Covered Systems:

- HVAC (heating and cooling)

- Plumbing systems

- Electrical systems

- Water heaters

Covered Appliances:

- Refrigerators

- Ovens and cooktops

- Built-in microwaves

- Dishwashers

- Washers and dryers

Optional Add-Ons (varies by provider):

- Pool and spa equipment

- Well pumps

- Septic systems

- Roof leak repairs

- Sprinkler systems

- Garage door opener

- Sump pumps, and more.

Many of the best home warranty plans, including First Premier, offer these add-ons to extend coverage beyond standard inclusions. It allows homeowners to tailor protection based on their property’s specific needs.

4. Saves Time and Effort

A warranty replaces a fragmented repair process with a single, coordinated workflow. Instead of researching contractors, comparing quotes, and managing schedules, you submit one request, and your job is done. The provider handles the rest, from technician assignment to repair approval, often within 24–48 hours.

The real advantage isn’t just speed. It is the removal of the stress of constant decision-making. There is no back-and-forth with multiple vendors or uncertainty around timelines and costs. For homeowners balancing work and home responsibilities, especially in older properties, this streamlined approach reduces ongoing effort. It keeps maintenance from turning into a recurring time drain.

5. Increases Your Home's Appeal to Buyers

Selling a home involves proving that the property is in excellent condition. Including a warranty in the listing acts as a powerful marketing tool. It signals to potential buyers that the systems are protected and well-maintained.

For homeowners looking to sell, a warranty can be a deciding factor for cautious buyers. It provides them with a safety net for their first year of ownership. This added layer of trust often leads to smoother negotiations and a faster closing process.

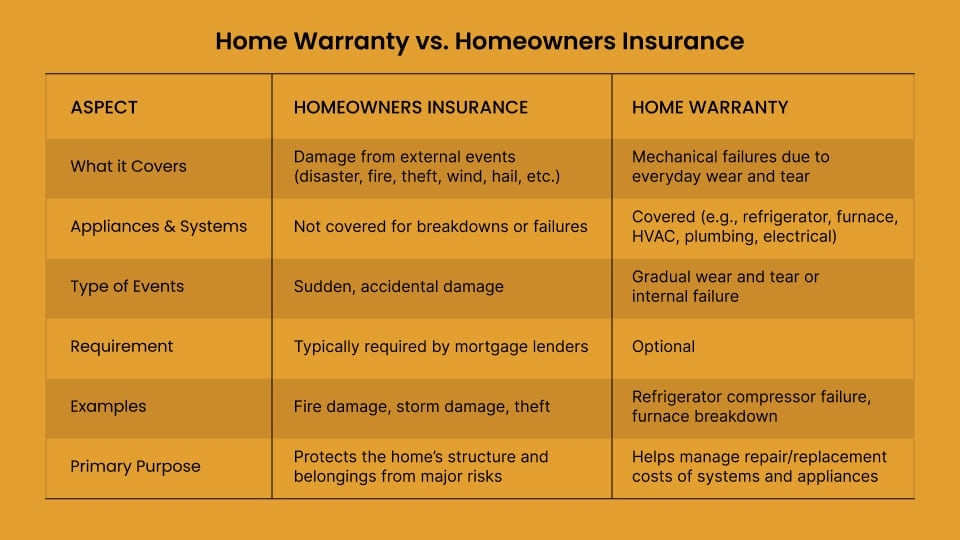

Home Warranty vs. Homeowners Insurance: What is the Difference?

This comparison trips up many buyers. It is not an either/or decision because these two cover completely different situations.

Homeowners insurance protects your structure and personal belongings from disaster, fire, or theft. A warranty protects your systems and appliances from aging and breakdown. Many financial advisors recommend having both. They are complementary, not redundant.

Are Home Warranties Worth It? Real Costs vs. Real Savings

This is the question every homeowner asks. The honest answer depends on your home's age, condition, and your personal risk tolerance.

According to a recent 2026 report by Market Reports World, the United States continues to see the highest adoption of home warranty plans globally, with more than 40 million active policies. This growth is largely driven by the increasing rate of appliance breakdowns and the rising cost of repairs, pushing homeowners to opt for more comprehensive coverage.

The Real Math

A standard home protection plan costs between $300 and $600 per year. A single HVAC repair can cost $500–$2,000. A water heater replacement runs $1,000–$1,800. If you face even one major repair annually, the benefits of home warranty coverage typically outweigh the annual premium.

Older Homes Benefit Most

Systems and appliances degrade over time. If your HVAC unit is 10+ years old or your water heater is approaching the end of its lifespan, the likelihood of a breakdown increases significantly. A warranty in this situation provides strong value.

New Homeowners and First-Time Buyers

Moving into a new home is already expensive. You may not know the full history of the appliances or systems. A home appliance warranty bridges that uncertainty.

What Reduces the Value?

If your home is newly built with all-new systems and appliances, and everything carries an active manufacturer's warranty, a home protection plan may offer less immediate value. Still, many homeowners choose it for the convenience alone.

How Do You Choose the Right Warranty Provider?

Not all home warranty providers offer the same level of service. The right choice often comes down to how easy they make things when something actually breaks.

Key Factors to Evaluate

- Coverage level: A balanced plan that protects systems and appliances, so you are not managing separate coverage gaps.

- Service call fee: Is the fee predictable and clearly defined? You need to see whether there is a flat, transparent fee with no surprises at the time of service.

- Claim response time: Prompt scheduling and assigning of a technician, ideally within a day or two of raising a claim.

- Coverage caps: Clearly stated limits that still cover the majority of typical repair costs.

- Contract terms: Simple terms with straightforward cancellation or adjustment options.

- Customer reviews: Check whether customers mention smooth claims and reliable service of the warranty provider. Consistent feedback around ease of use and responsiveness sets a provider apart.

Compare the Plans Side by Side

Many comparison sites allow you to filter by state, coverage type, and budget. The home warranty benefits become clearest when the fine print matches what was advertised.

If you are looking for a provider that offers transparent coverage and responsive claims support, First Premier Home Warranty is worth a close look. With flexible warranty plans covering both systems and appliances, we protect homeowners from the financial impact of unexpected breakdowns. Today, we are recognized among the best home warranty in the USA.

See what your home actually needs coverage for. Call 1-800-388-1918 for a personalized quote.

Frequently Asked Questions

How do you file a home warranty claim?

You can file a claim online through your customer portal or by calling your provider. Once submitted, a technician is assigned, usually within 24–48 hours.

Does a home warranty cover all appliances?

No, coverage depends on the plan. Basic plans cover major appliances, while comprehensive plans include additional systems and optional add-ons.

Is a home warranty transferable when selling a home?

Yes, most home warranties are transferable to the new homeowner. This can increase buyer confidence and support a smoother sale.

Are pre-existing conditions covered under a home warranty?

No, most home warranty plans do not cover pre-existing conditions. Issues must occur after the coverage begins to be eligible.

Do all homes qualify for a home warranty?

Yes, most property types qualify, including single-family homes, condos, townhouses, and rental properties. Eligibility may vary based on the provider.

What does a home warranty not cover?

Home warranties typically do not cover structural damage, cosmetic issues, or failures caused by misuse, neglect, or pre-existing conditions.

Related Posts

1-800-388-1918

Protect Your Property, Secure Your Peace: Your Plan Starts Here.